NPLs reduces to almost GHc7b – BoG report

The total stock of Non-Performing Loans (NPLs) reduced significantly to almost GHc7 billion ending June this year.

This was contained in the latest Banking Sector Report released by the Bank of Ghana. The data covered operations of all the banks in the country from June 2017 to June 2019.

The drop in the Non-Performing Loans represents a contraction of 20.0 percent compared with the 9.7 percent growth recorded a year earlier.

The decline in the stock of NPLs coupled with the marginal pick-up in credit growth translated into a lower NPL ratio of 18.1 percent in June 2019 from 22.6 percent a year ago.

According to Bank of Ghana when adjusted for the fully provisioned loan loss category, the NPL ratio declined to 9.0 per cent from 12.3 percent, signalling a slowdown in deterioration of loan quality.

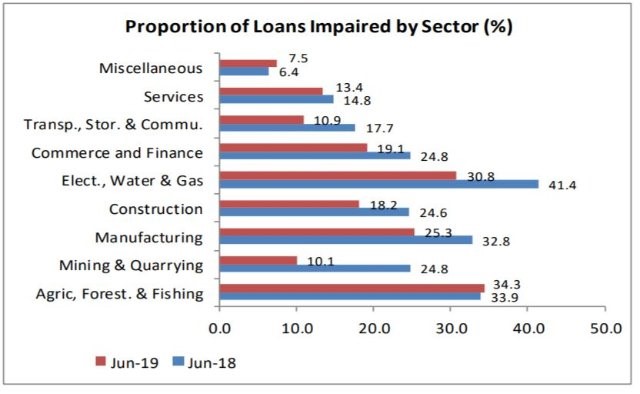

Breakdown of the NPLs

The report showed that 97 per cent of this Non Performing Loans were credit given to persons and businesses in the private sector, up from the 89.9 percent recorded in June 2018, while the public sector’s contribution declined to 2.4 per cent from 10.1 per cent over the same comparative period.

Indigenous private enterprises accounted for 74.6 percent of total NPLs in June 2019, slightly below the 75.4 percent share recorded in the same period in 2018, while the contribution of foreign enterprises increased to 9.0 per cent from 7.5 percent.

The share of households in industry NPLs increased from 6.3 per cent to 11.7 per cent during the period under review, partly due to their increasing share of industry credit.

The services sector, the second-highest recipient of the industry’s credit also had the second-highest share of the industry’s NPLs of 16.4 per cent.

Manufacturing and electricity, water and gas sectors had respective shares of 16.2 per cent and 15.6 per cent of the industry’s impaired loans.

The lowest recipient of banking industry credit, mining and quarrying, also had the least share of industry NPLs of 2.0 per cent. Overall, the top three largest contributors to the industry’s NPLs commerce & finance.

Drivers of the reduction

According to the Bank of Ghana, Asset quality improved as the industry’s NPL ratio declined in June 2019 compared with the same period last year.

This was on the back of implementation of Bank of Ghana’s loan write-off policy as well as loan recovery efforts by banks.

As banks continue to align credit risk frameworks with the new Capital Requirement Directive issued in 2018, credit risk exposure is expected to decline further.

Impact of the NPLs reduction

For some analysts might be good when looking at the books of these banks. However, since it’s not businesses paying back these loans, it could still impact negatively on the cost of credit going forward.

This is because some banks would still find why price these “bad” loans into fresh loans going forward.

This could increase the cost of credit, a development that most industry players and regulator are hoping could go down as a result of the recent development in the economy.

Banks Profitability ending June this year

The profitability indicators of the banking sector improved during the first half of 2019 compared with the same period last year, according to the Bank of Ghana.

The industry recorded an after-tax profit of GH¢1.67 billion, representing year-on-year growth of 36.3 per cent compared with 21.7 per cent in the same period last year.

The strong profit performance was underpinned by higher growth of net interest income. Net interest income grew by 20.7 percent reflecting both higher interest income from investments and lower interest expenses from reduced borrowings.

Net fees and commissions grew by 3.7 percent, significantly below the 24.7 percent growth for the same period last year, attributable to the slowdown in the volume of off-balance sheet activities.

Loan performance June ending 2019

Gross loans and advances (excluding loans under receivership) was GHc38.7 billion in June 2019, unchanged from June 2018.

The Bank of Ghana argued that in real terms, gross loans and advances contracted by 8.4 per cent in June 2019, reflecting the impact of the loans under receivership, compared to the 6.3 percent contraction in June 2018.

In nominal terms, the stock of credit to the private sector (comprising private enterprises and households) grew by 1.9 percent to GHc35.08 billion in June 2019 compared with the 4.8 percent annual growth in June 2018.

In real terms, private sector credit (excluding those under receivership) contracted by 6.6 per cent in June 2019 compared with a contraction of 4.7 per cent a year ago.

Breakdown of loans disbursed

Credit to households amounted to GH¢8.41 billion in June 2019 compared with GHc6.29 billion in the same period last year, indicating an annual growth of 10.5 per cent.

Real growth in credit to households was 1.3 per cent in June 2019, lower than the 11.9 per cent growth in June 2018 The share of private sector credit increased marginally to 90.7 percent in June 2019 from 88.9 per cent in June 2018.

Of the total, the share of private enterprises was 66.4 percent in June 2019 compared with 67.6 percent a year ago.

The proportion of households’ credit in the industry’s credit increased to 21.7 percent in June 2019 compared with 19.6 percent a year ago, while the share of credit to ‘other’ private entities increased to 2.5 percent from 1.7 per cent during the same comparative period

Deposits mobilization

Based on the report deposits during the year under review was also doing well. According to the Bank of Ghana’s data deposits increased by 22.3 percent to GHc75.57 billion as at end-June 2019.

Both domestic and foreign currency deposits outperforming the previous year’s performance. The robust growth in deposits, according to the Bank of Ghana reflects increasing confidence and stability in the banking sector following the reforms.

Domestic deposits, the largest component of total deposits grew by 22.5 percent on an annual basis to GHc75.2 billion compared with 13.4 percent growth a year ago.

Foreign currency deposits also grew strongly by 37.9 percent in June 2019 to GHc21.63 billion against 6.8 percent growth recorded in June 2018, partly attributed to the depreciation of the Ghana Cedi.

The sustained growth in deposits pushed its share of the banking sector’s pool of funds from 61.6 percent to 67.0 percent during the period under review.

State of the Banking Sector

The Bank of Ghana also argues that the half-year performance showed that the banking sector was well-capitalised, solvent, liquid and profitable with improved financial sector indicators. Asset growth remained strong underpinned by sustained growth in deposits and higher capital levels.

The Central Bank says credit growth post-re-capitalisation continued to pick up alongside increased after-tax profits, adding that “Key Financial Soundness Indicators (FSIs) also improved in response to the banking sector reforms,” Ghana Capital Requirement Directive (CRD) under the Basel II/III capital framework remained well above the statutory minimum of 10 per cent and 13 percent respectively, pointing to increased resilience of the sector following the recapitalisation.

Outlook for the banking sector

The regulator of the banking sector Bank of Ghana in the report maintained that the banking sector is expected to remain strong with continued improvement in the key FSIs. Deposits growth is also projected to remain robust and together with the higher capital levels, drive credit growth.

Going forward, improved financial intermediation will be supported by sustained efforts aimed at reducing the industry’s stock of NPLs through write-offs, recoveries and intensified credit risk management practices on the part of the banks.

Latest Posts

157TH Canada Day Celebration: Celebrating Strong Bilateral Trade between Canada and Ghana

July 01, 2024

FATHER’S DAY DINNER WITH PRINCE KOFI AMOABENG

July 01, 2024

FREIGHT FORWARDERS AND LOGISTICS SECTOR MEETING

July 01, 2024

Celebrating Women at the Mother’s Day Dinner

June 03, 2024

CANCHAM Pharmaceutical Sector Meeting Highlights

June 03, 2024

In-house Presentation (May Edition)

June 03, 2024

CANCHAM ANNUAL GENERAL MEETING

May 08, 2024

Construction Sector Meeting Hosted by CANCHAM

May 08, 2024

INDUSTRIAL TOUR TO MERIDIAN PARK BY LMI HOLDINGS

May 08, 2024

A JAZZ AND WHISKY AFFAIR: A Tri-Chamber Collaboration!

May 08, 2024

May 08, 2024

EMPOWERING THE FUTURE: ALINEA FOUNDATION’S WEE-NORTH PROJECT AGM

April 04, 2024

EMPOWERING CHANGE: CANCHAM AND JOY BUSINESS INTERNATIONAL WOMEN’S DAY DIALOGUE

April 04, 2024

April 04, 2024

EXPLORING FLAVORFUL HORIZONS: A JOURNEY WITH FREDDIE BEVERAGES

April 04, 2024

EXPLORING HORIZONS: INSIGHTS FROM HOLLARD INSURANCE’S JOURNEY

April 04, 2024

UNLOCKING OPPORTUNITIES: SENA CHARTERED SECRETARIES LIMITED’S EXPANSION ENDEAVOR

April 04, 2024

Highlights from CANCHAM Chocolate Day Member Forum 2024

March 01, 2024

TVET Workshop by Canadian High Commission in Collaboration with CANCHAM

March 01, 2024

Unlocking Potential: Insights from Asante-Chirano

March 01, 2024